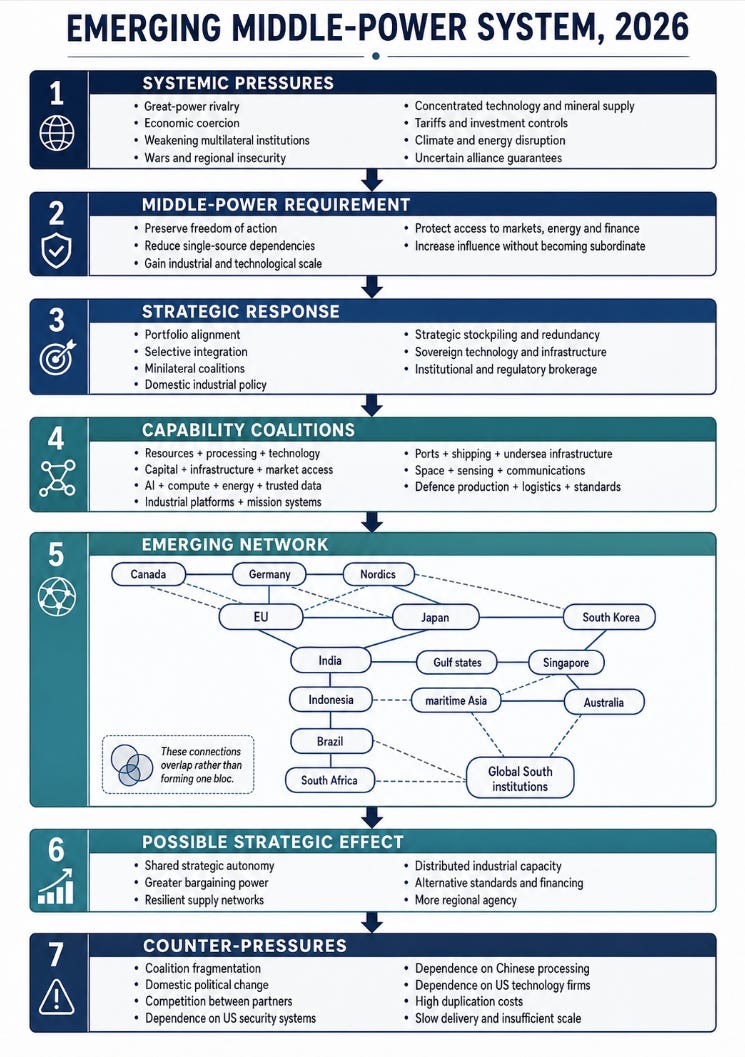

Middle powers in 2026

The emerging networked middle-power system

What is emerging is not a stable third bloc between the United States and China.

It is a networked middle-power system made up of overlapping, capability-specific coalitions. Countries cooperate where their assets are complementary, compete where their industries overlap, and remain dependent on one another in areas they cannot control alone.

Middle-power influence is shifting from diplomatic status to functional control over strategic systems.

A country matters increasingly because it controls, supplies, finances, connects, protects or regulates something others cannot easily replace.

That could be:

minerals and energy

AI models, compute or data

industrial production

capital and project financing

ports, maritime routes and Arctic access

aerospace and space capabilities

standards, certification and market access

logistics and infrastructure

diplomatic access across competing blocs

The result is best understood as portfolio alignment. Countries maintain several overlapping partnerships rather than making one permanent geopolitical choice.

What is driving the change

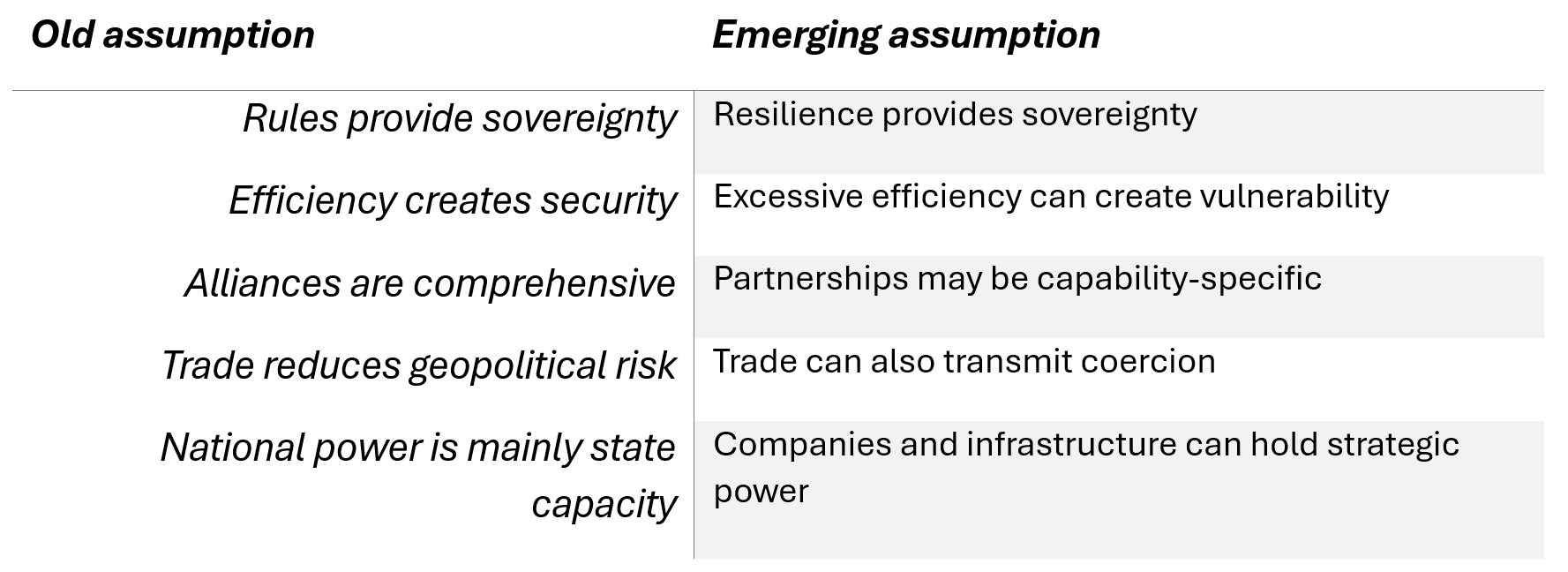

Rules are no longer considered sufficient protection

Middle powers traditionally relied on institutions, international law and predictable access to global markets. Those mechanisms remain important, but countries increasingly doubt that they will prevent tariffs, export controls, financial pressure, technological denial or supply interruption.

Canada’s January 2026 middle-power doctrine captured this directly. Prime Minister Mark Carney argued that integration itself can become a source of vulnerability and that countries are therefore seeking greater autonomy in energy, food, critical minerals, finance and supply chains. He also argued that collective resilience is less costly than every country attempting complete self-sufficiency.

This produces an important distinction:

The system is not simply deglobalizing. Global trade reached approximately $35 trillion in 2025, while new connector economies expanded trade with multiple competing centres. The deeper change is rerouting and restructuring, not the disappearance of international integration.

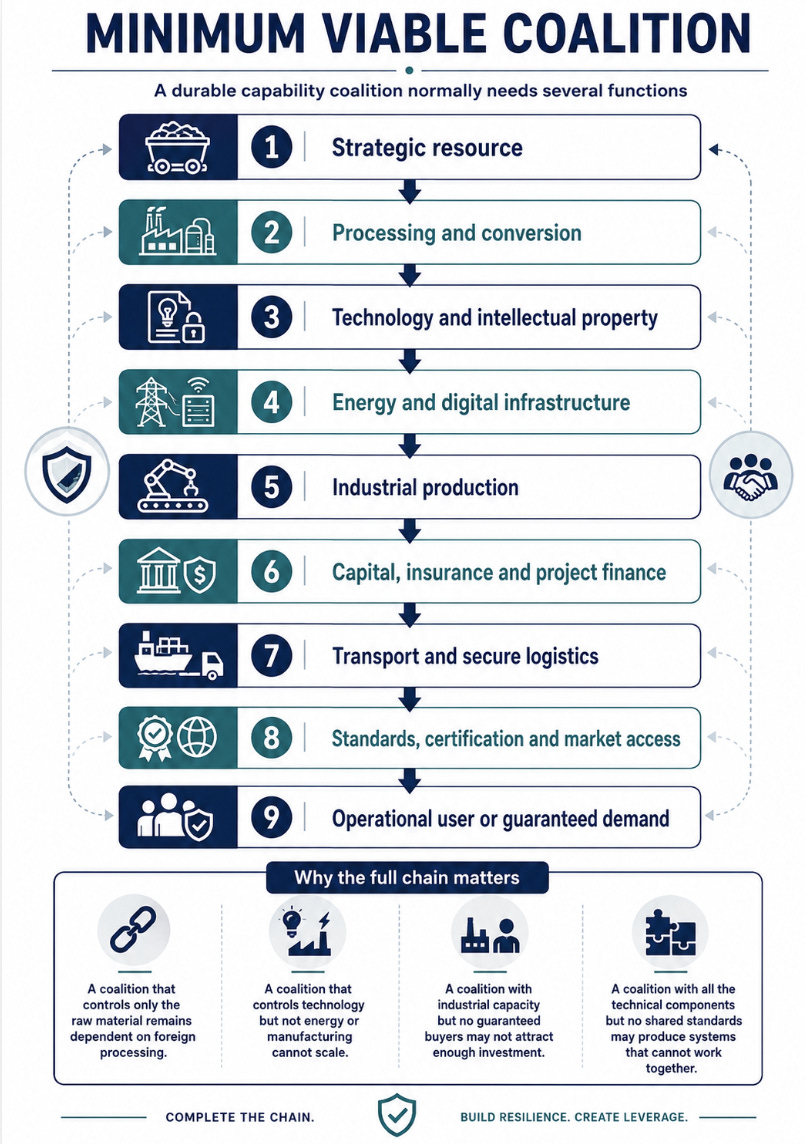

The new unit of power is the capability stack

Middle powers rarely control an entire strategic value chain. They gain influence by combining complementary pieces.

What minimum viable coalition can control enough of the full chain to withstand outside pressure?

The principal middle-power archetypes

Countries occupy different positions in the emerging system. Many belong to more than one category.

Industrial platform powers

Germany, Japan, South Korea, Sweden, Poland, the Netherlands and increasingly Türkiye

Their influence comes from manufacturing, engineering, specialized firms, production knowledge, industrial standards and integration into advanced supply chains.

Their central problem is that industrial capability may depend on imported energy, critical minerals, semiconductors, software or external markets.

Their preferred coalitions connect industrial capacity with resource producers, technology ecosystems and reliable export markets.

The EU–Japan Competitiveness Alliance illustrates this model. It links critical minerals, semiconductors, energy, defence, space, research and digital cooperation rather than treating trade, security and technology as separate policy areas.

Resource and energy powers

Canada, Australia, Norway, Saudi Arabia, the United Arab Emirates, Brazil, Indonesia and Chile

These states possess minerals, energy, land, renewable potential or processing leverage. Their strategic objective is increasingly to move beyond extraction into refining, manufacturing, technology and ownership.

Indonesia demonstrates how resource control can be converted into industrial leverage. Its position in nickel has increased its bargaining power with both Chinese and Western industrial systems. The IEA reports that Indonesia accounted for most recent growth in nickel refining, while mineral processing more broadly remains highly concentrated.

The danger for these countries is remaining upstream suppliers in someone else’s industrial system.

Technology and knowledge powers

Canada, South Korea, Singapore, Israel, Sweden, Finland, the Netherlands and parts of India

Their leverage comes from AI research, advanced engineering, digital infrastructure, semiconductor equipment, telecommunications, cybersecurity, robotics or specialized talent.

But technological power is highly layered. Having AI researchers does not automatically provide control of advanced chips, fabrication, cloud infrastructure, data centres, electricity, foundational models, capital, deployment platforms

The 2026 AI Index identifies a sharply concentrated system. The United States hosts far more data centres than any other country, while one Taiwanese foundry fabricates almost all leading AI chips. At the same time, South Korea leads in AI patents per capita and China and the United States hold different advantages across research, models, patents and industrial robotics.

This creates a growing group of technological swing states that possess valuable pieces of the AI system without controlling the entire stack.

Capital and infrastructure powers

The UAE, Saudi Arabia, Singapore, Qatar and Norway

These actors can translate sovereign capital, infrastructure investment, energy and logistics into strategic influence.

They can finance projects that industrial and resource powers cannot fund independently. They can also connect Western technology, Asian manufacturing and Global South markets.

Their influence comes partly from their ability to operate across political systems rather than entering one exclusive bloc.

Geographic and logistical bridge powers

Türkiye, India, Indonesia, Saudi Arabia, the UAE, South Africa, Singapore and Canada

These countries sit between regions, maritime routes, energy systems or political groupings.

Their territory, ports, air corridors, Arctic access, undersea infrastructure or diplomatic reach make them difficult to bypass.

Their power rises when:

shipping routes become less secure

sanctions redirect trade

supply chains require alternative corridors

allies need access to distant theatres

regional crises interrupt normal routes

However, connector status is not automatically safe. IMF research finds that countries benefiting from redirected trade may become more exposed to later fragmentation, retaliation or demand shifts.

Institutional brokers

Canada, Japan, India, Brazil, Indonesia, South Africa and Singapore

These states participate in multiple institutions and can translate ideas between different groups.

India, for example, can participate in the Quad, BRICS, the G20 and partnerships with Europe and the Gulf without treating any one relationship as exclusive. The January 2026 EU–India partnership expanded cooperation across maritime security, technology, space, defence industry, cyber and connectivity.

BRICS is also expanding as a venue for bargaining over financing, local-currency transactions and Global South representation. Its membership and internal diversity suggest that it is better understood as a negotiation and option-building platform than as a cohesive strategic alliance.

What the emerging coalitions look like

Coalition type one

Trusted industrial complementarity

Countries combine resources, technology, capital and manufacturing because none can achieve strategic scale independently.

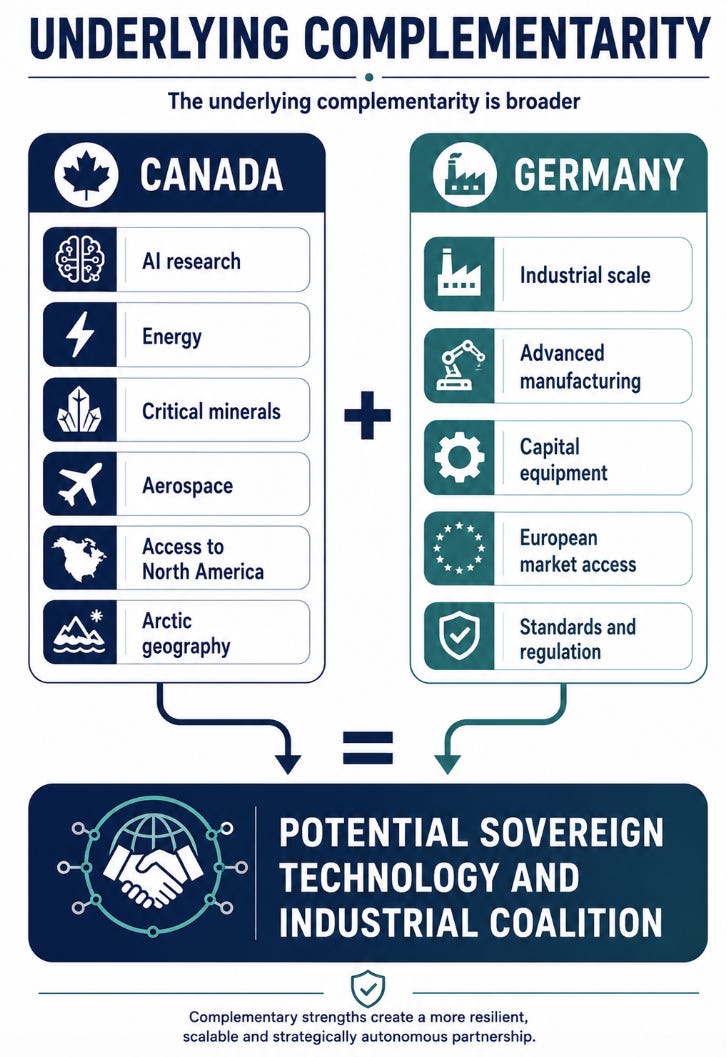

The February 2026 Canada–Germany Sovereign Technology Alliance is an early example. It connects secure compute, AI research, commercialization, skills and resilient digital infrastructure while explicitly seeking to reduce strategic technology dependencies.

The underlying complementarity is broader:

The coalition matters only if it advances from declarations to shared infrastructure, financed projects, commercial demand and deployable capability.

Coalition type two

Cross-regional security-industrial partnerships

Europe and the Indo-Pacific increasingly view their security environments as connected.

EU–Japan and EU–India arrangements now combine economic security with maritime, cyber, space, industrial and technological cooperation. These are not traditional military alliances. They are cross-regional resilience partnerships.

They reflect a wider recognition that European security depends on Indo-Pacific production and trade and Indo-Pacific security depends on European markets, technology and diplomatic support.

Coalition type three

Resource-to-industry coalitions

These bring together resource producers and industrial consumers.

The objective is not simply reliable supply. It is shared control of extraction, processing, recycling, component production, standards, long-term purchasing, project finance.

This is urgent. The top three refining countries controlled approximately 86 percent of refining for major energy minerals in 2024, up from roughly 82 percent in 2020. Around 90 percent of supply growth came from the leading supplier, principally China across most minerals and Indonesia for nickel.

There is not one fixed set of three countries behind the 86% figure. The IEA calculated the top three refiners separately for each mineral, copper, lithium, nickel, cobalt, graphite and rare earth elements and then averaged their combined shares.

The clearest country-level picture is:

China is the leading refiner for copper, lithium, cobalt, graphite and rare earth elements.

Indonesia is the leading refiner for nickel.

No single third country. The other leading positions vary by mineral, involving countries such as Chile, Japan, Argentina and others.

Canada has consequently established or expanded critical-mineral mechanisms with Germany, Australia, Saudi Arabia, Japan, South Korea, the EU, Chile and others.

Coalition type four

Sovereign AI networks

The emerging AI coalition is not simply a group of countries building national language models.

It involves shared access to trusted models, compute, electricity, data, cloud infrastructure, advanced chips, talent, safety and evaluation systems, procurement demand, interoperable governance.

Few middle powers can build this stack nationally. Their realistic route is federated technological sovereignty, where countries share infrastructure and standards while retaining authority over data, models and sensitive applications.

This could become one of the defining middle-power coalition spaces between 2026 and 2030.

Coalition type five

Capital-resource-technology triangles

Gulf states increasingly connect western technology, Asian industrial capacity, energy and land, sovereign investment, access to African and South Asian markets.

These are not merely bilateral relationships. They are often triangular or quadrilateral arrangements.

Technology state -> Gulf capital and energy -> Resource or market state -> Industrial production partner

This gives the Gulf states influence far beyond their population size. Their role is shifting from energy supplier to capital allocator, infrastructure owner and technology platform host.

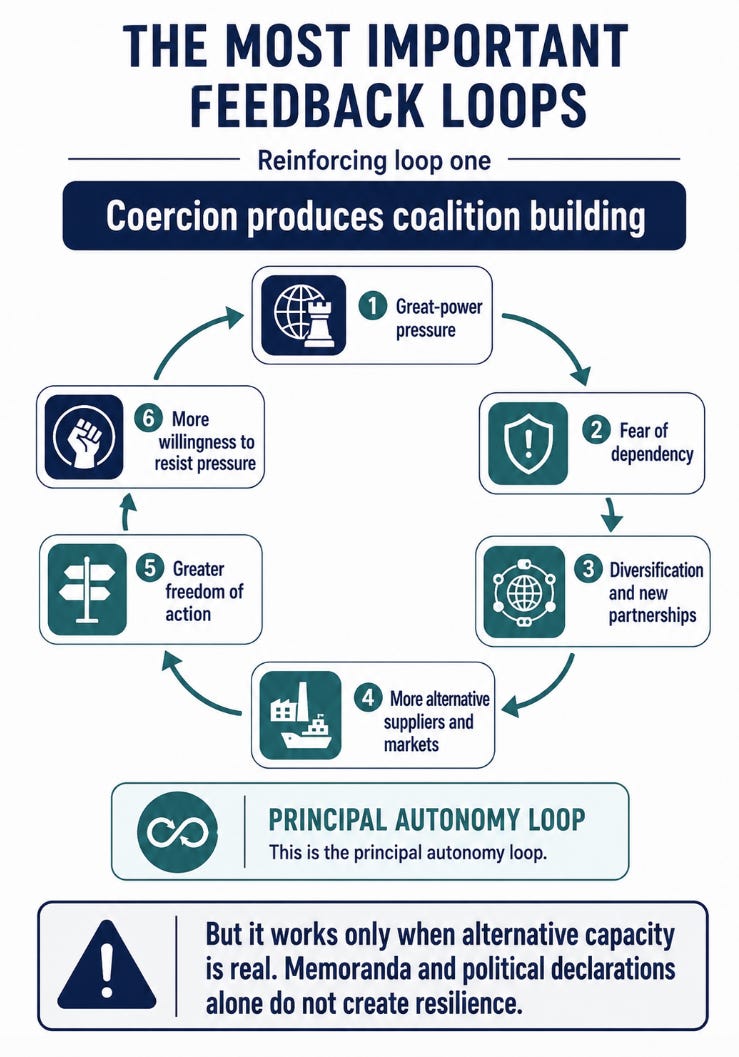

Reinforcing loop one.

Reinforcing loop two

Capability attracts capability

Initial strategic asset -> Foreign investment -> Domestic infrastructure and skills -> Higher-value production -> Greater bargaining power -> More investment

Indonesia’s nickel strategy demonstrates this potential, although it also illustrates the risk that domestic industrial development may remain heavily dependent on foreign capital and technology.

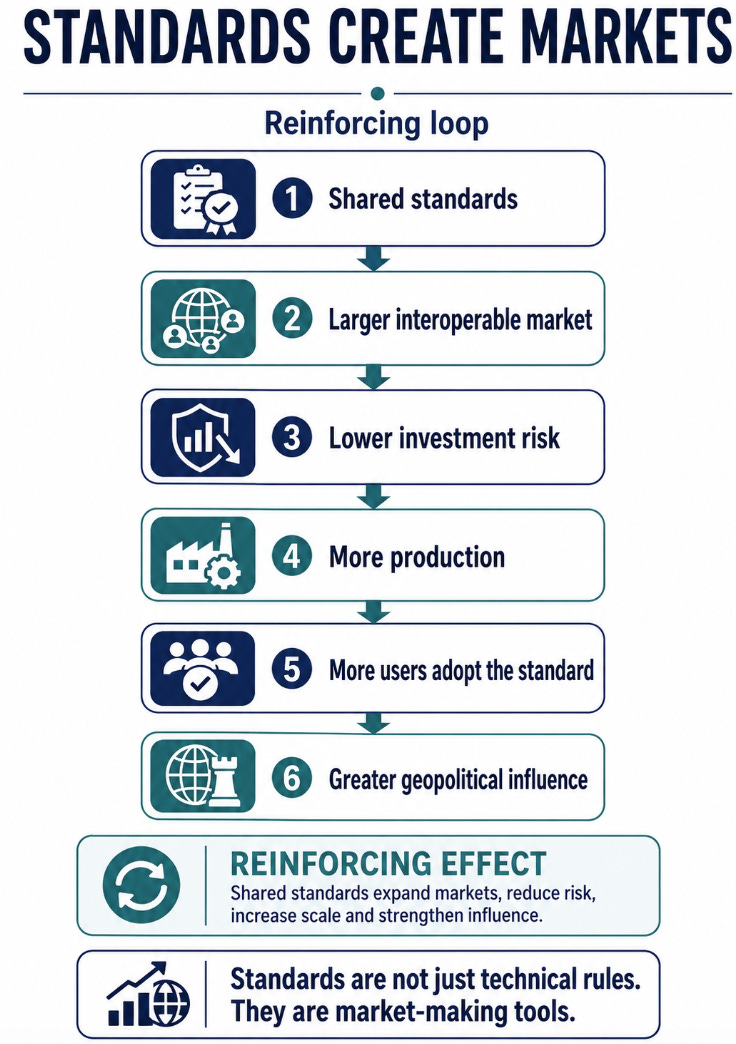

Reinforcing loop three

Standards create markets

This is why certification, data rules, AI governance, environmental standards and interoperability can have effects comparable to conventional industrial policy.

Balancing loop one

Autonomy is expensive

More redundancy and domestic capacity -> Higher costs -> Fiscal and political pressure -> Reduced investment -> Continued dependency

Not every supply chain can or should be reproduced domestically. The strategic challenge is identifying which dependencies are genuinely intolerable and which can be managed through diversification.

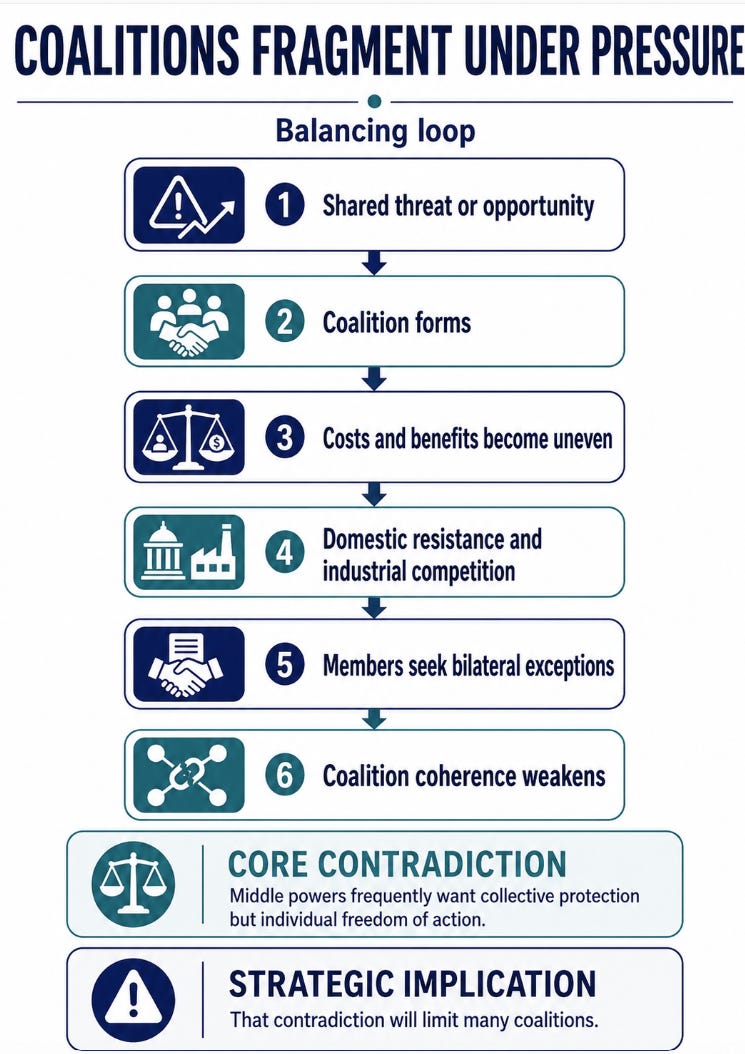

Balancing loop two

Coalitions fragment under pressure

Middle powers frequently want collective protection but individual freedom of action. That contradiction will limit many coalitions.

Balancing loop three

The hidden great-power dependency

A coalition may appear autonomous while still depending on:

US security guarantees

US cloud and AI firms

Chinese mineral processing

Taiwanese semiconductor fabrication

European regulatory access

dollar-based finance

This means that some middle-power coalitions will diversify dependencies rather than eliminate them.

The emerging regional laboratories

The Arctic

The Arctic is becoming a test of whether middle powers can integrate sovereignty, infrastructure, Indigenous partnership, sensing, energy, logistics and industrial capability.

Canada, Norway, Finland, Sweden and Denmark possess different but complementary assets. The region could produce capability coalitions around:

communications and sensing

resilient infrastructure

energy and minerals

aerospace and maritime awareness

cold-weather mobility

civil-military logistics

trusted data and AI

The Arctic therefore connects security, climate, economic development and infrastructure in one system.

The Indo-Pacific

The Indo-Pacific is the most advanced laboratory for portfolio alignment.

Japan, India, Australia, South Korea, Indonesia and Singapore simultaneously maintain:

US security relationships

economic links with China

regional institutions

bilateral technology agreements

independent industrial strategies

This is not indecision. It is deliberate risk management.

The Gulf and wider Middle East

The Gulf demonstrates how energy and capital powers can acquire technological and geopolitical agency.

Saudi Arabia, the UAE and Qatar are increasingly able to choose among American, European, Chinese, Indian and other partners. Their decisions influence AI infrastructure, energy transitions, logistics, financing and regional diplomacy.

Europe

European middle powers are moving from being principally consumers of collective security toward becoming industrial and capability producers.

Military spending in Europe rose by 14 percent in 2025, while spending in Asia and Oceania increased by 8.1 percent. Germany, Poland, Japan, Australia, South Korea and other states are consequently gaining more weight within their respective alliance systems.

The strategic question is whether higher spending becomes fragmented national capacity or interoperable strategic mass.

The deepest emerging pattern

The middle-power landscape is becoming a multiplex network.

A country can be:

allied with another country militarily

dependent on it technologically

competing with it industrially

cooperating with it on critical minerals

divided from it on trade

partnered with it in a third region

This means the future system is unlikely to divide neatly into aligned and non-aligned countries. It will consist of overlapping coalitions in which countries cooperate in one domain, compete in another and remain dependent on each other in a third.

The central contest will therefore be less about recruiting countries permanently into one camp and more about determining:

Which coalition controls each critical capability.

Which standards its members adopt.

Where infrastructure and production are located.

Who provides the capital.

Who owns the data and intellectual property.

Who has guaranteed access during a crisis.

Who can exit the arrangement without unacceptable costs.

Four plausible pathways to 2030

Pathway one - Networked strategic autonomy

Middle powers build functioning coalitions across AI, minerals, energy, infrastructure and industrial production.

They remain allied with larger powers but become less vulnerable to sudden policy changes.

This is the most positive pathway.

Pathway two - Competitive capability clubs

Coalitions form, but access becomes conditional.

Trusted groups create separate technology, industrial and financial systems. Middle powers gain resilience inside their clubs but lose access outside them.

This would produce partial bloc formation without two completely separate global economies.

Pathway three - Connector-state ascendancy

India, the Gulf states, Indonesia, Türkiye, Brazil and others gain influence by linking competing economic systems.

Their bargaining power rises, but so does pressure from larger powers to choose sides.

The decisive variable will be whether they develop domestic production or remain routes through which other powers trade.

Pathway four - Fragmented sovereignty

Middle powers announce numerous alliances but fail to finance or implement them.

Dependence remains concentrated, costs rise, projects are duplicated and domestic political changes repeatedly interrupt cooperation.

Under this pathway, the language of strategic autonomy expands faster than actual capability.

The strategic insight for Canada and NATO

The opportunity is not to create a formal alliance of middle powers.

It is to become an architect and indispensable node of capability coalitions.

Canada’s most useful assets are not isolated national strengths. They are the combinations it can offer:

AI + energy + secure compute

Critical minerals + trusted standards + market access

Arctic geography + sensing + infrastructure

Aerospace + European and Nordic mission technologies

Research + allied industrial production

North American access + European partnerships

NATO membership + Indo-Pacific relationships

For NATO, the challenge is to turn a growing web of bilateral and minilateral partnerships into real collective capability. That means connecting nationally owned forces, industrial capacity, data, infrastructure and technology so they can produce greater scale, resilience and operational effect together, without requiring every initiative to be absorbed into a single centrally controlled alliance system.

The advantage will come from federation of common standards, interoperable interfaces and shared objectives, combined with distributed ownership and national freedom to contribute at different levels.

Federated capability coalitions with common outcomes, interoperable interfaces and distributed national ownership.

Final assessment

The middle-power moment of 2026 is not primarily a diplomatic movement.

It is the early formation of a new operating system for international power.

Its basic unit is the capability coalition.

Its organizing behaviour is portfolio alignment.

Its strategic objective is decision sovereignty.

The principal source of influence is control of an indispensable function within a wider network.

And its central vulnerability is that most middle powers are still trying to construct autonomy using infrastructure, technology, finance and security systems controlled by the great powers.